A Package for Backtesting Options Strategies on QuantConnect or Simulated Data

An explanation as to why options strategy backtesting is useful and why I recommend using Options Backtest

6/12/20234 min read

Introduction

Retail traders often struggle to make consistent profits due to a lack of a systematic approach to trading. Studies show that the amount of retail traders that experience net losses ranges from 80% to 97% over various timeframes [1–4]. In contrast, the S&P 500 offers an average annual gain of approximately 9%, requiring minimal monitoring [5]. The challenges in retail trading arise from biases prevalent in the industry, including survivorship bias, confirmation bias, and overconfidence bias [6,7]. Overcoming these biases necessitates treating trading strategies like scientific experiments. By rigorously adhering to the scientific method, traders can dramatically increase their chances of being in that profitable minority.

Understanding Backtesting and Its Importance

Backtesting serves as a critical step in developing and evaluating trading strategies. It involves testing a strategy against historical or simulated market data to assess its performance. Through the use of controlled, objective, and repeatable datasets, traders gain valuable insights into the strengths, weaknesses, and overall effectiveness of their strategies.

The Benefits of Rigorous Backtesting

Rigorous backtesting offers several key benefits that significantly improve options trading:

Strategy Validation: Backtesting validates a strategy’s effectiveness across different market conditions through empirical evidence of its historical performance, helping identify potential pitfalls and hidden opportunities.

Risk Assessment: Backtesting allows traders to use historical data to evaluate the risks associated with their options strategies, enabling them to calculate maximum drawdowns, volatility, and risk-adjusted returns for informed decision-making and effective risk management.

Iterative Improvement: Backtesting facilitates an iterative approach to strategy development, allowing traders to continuously analyze strategy performance, identify areas for improvement, and enhance their trading performance.

Egoless Live Implementation: Once traders code the strategy for a backtest, they can simply port it into a trading bot for live or forward testing, avoiding the cognitive biases and time demands that inhibit the exact execution of the strategy.

The Benefits of Options

Trading options, instead of the underlying stock, can be useful for several reasons:

Income Generation: A trader sells options to generate income, receiving a small premium in return for the risk of loaning out their 100 shares (a covered call) or the cash to buy 100 shares (a covered put). If the underlying stock price lands favorably at expiration time, either below the strike for a covered call, or above the strike for a covered put, the option becomes worthless and the trader retains their full deposit.

Leverage: For a small upfront price (the option premium), traders command a larger amount of underlying stock for a brief period. This leverage magnifies potential gains if the stock moves favorably.

Hedging: Investors use stock options as a risk management tool. Those owning a particular stock buy put options to guard against a potential price decline. If the stock price falls, the value of the put option rises, counterbalancing the stock position losses. It’s like buying insurance for your stocks.

Portfolio Diversification: Investors use options to add another layer of diversification to their portfolios. With options strategies, they manage risk and potentially increase returns in various market conditions.

Options Backtest: a Python Package for Backtesting of Options Strategies

To simplify the backtesting process, I developed a powerful but user-friendly Python package. It provides comprehensive tools and functionalities that empower traders to analyze and optimize their options trading strategies.

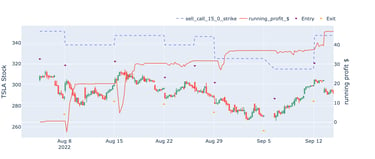

The return of a weekly iron condor strategy. During this sideways market, this strategy consistently returned a profit

Key Features of Options Backtest:

Historical and Simulated Data: It enables backtesting on both true options historical data from QuantConnect as well as options prices derived from the Black Scholes model. Any date range can be selected to prevent recency bias. This flexibility enables the analysis of strategy performance under various market conditions.

Strategy Customization: It offers easy customization and implementation of complex options trading strategies with several legs and different expiration dates. Whether testing poor man’s covered calls, straddles, or spreads, the flexible framework facilitates modeling and evaluation. Early stop and start criteria are also available.

Performance Metrics and Visualization: It provides a wide range of performance metrics, including profitability, risk-adjusted returns, and drawdown analysis. Additionally, intuitive visualizations such as equity curves, trade logs, and strategy comparisons aid in understanding strategy performance.

Parameter Optimization: Optimizing strategy parameters is crucial for maximizing profitability and reducing risk. The package includes advanced optimization algorithms that systematically explore parameter spaces with the Monte Carlo method, identifying optimal values for strategies.

Seamless Integration with QuantConnect: The code base mirrors the most commonly used classes in QuantConnect, allowing for offline development and testing of code. This means that when the code is deployed and a strategy is tested on historical data through QuantConnect, it seamlessly integrates out of the box.

Conclusion

Rigorous backtesting of options strategies is a vital step towards achieving profitable trading. By utilizing Options Backtest, traders can effectively evaluate and refine their strategies based on historical or simulated data. With its intuitive interface, comprehensive performance metrics, and powerful customization capabilities, this package equips traders with the tools necessary to enhance their options trading success.

Stay tuned for our upcoming blog posts, where I will delve deeper into the features and applications of the package, providing practical examples of backtesting options strategies. Prepare to elevate your trading prowess and unlock the full potential of options trading!

See repository here https://github.com/RupertDodkins/options_backtest

Bibliography